Introduction – Why This Matters

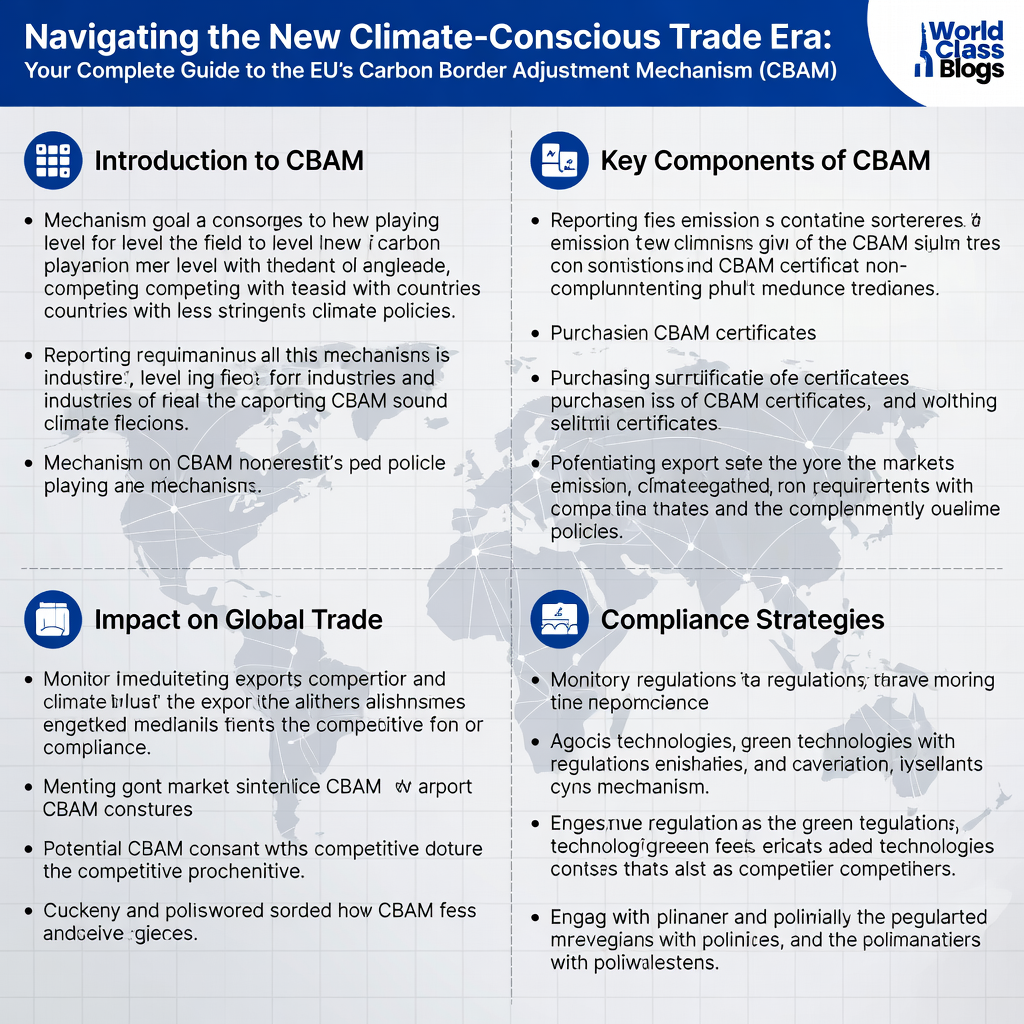

The landscape of global trade is undergoing its most significant transformation in decades, and it’s not being driven by a traditional trade war, but by a climate imperative. The European Union’s Carbon Border Adjustment Mechanism (CBAM) is more than a new regulation; it is a paradigm shift that places a concrete price on the carbon emissions embedded in the goods we trade. For curious beginners, it’s a fascinating case study in how environmental policy is becoming foreign and economic policy. For professionals needing a refresher, it’s an urgent compliance and strategic reality that is already reshaping sourcing decisions, cost structures, and competitive dynamics.

In my experience advising manufacturing firms, the initial reaction to CBAM is often one of anxiety—seen as just another complex, costly EU bureaucracy. However, what I’ve found is that companies that dive deep and understand CBAM’s mechanics are uncovering not just risks, but also opportunities for efficiency gains, product differentiation, and stronger supplier relationships. This isn’t merely about paying a tax; it’s about fundamentally understanding and managing the carbon footprint of your value chain.

By 2034, CBAM will cover over 50% of the emissions under the EU Emissions Trading System (ETS). Its ripple effects are prompting other economies, like the UK and Canada, to develop similar mechanisms. Understanding CBAM is no longer optional for any business or professional connected to global trade; it is essential literacy for the new, climate-conscious global economy.

Background / Context

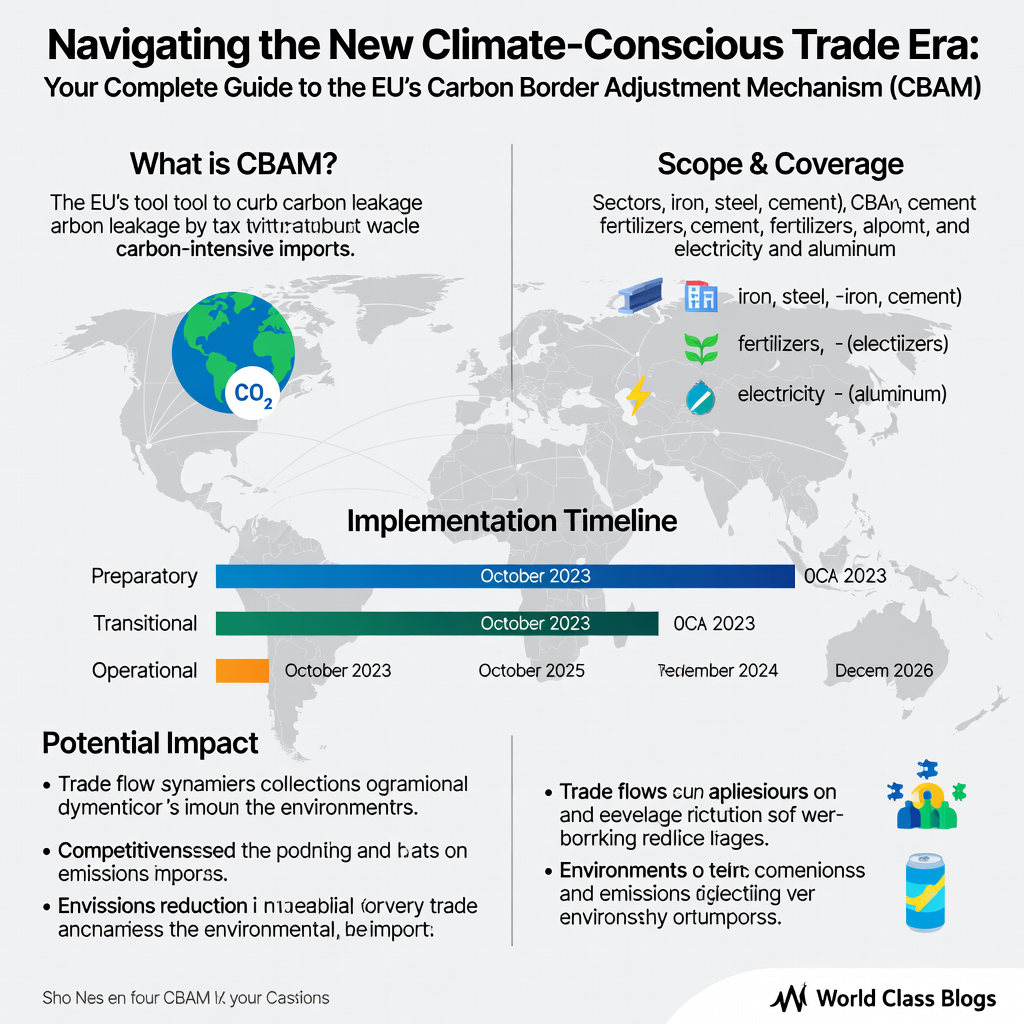

To understand CBAM, we must first understand the problem it aims to solve: carbon leakage. Carbon leakage occurs when companies based in the EU, facing strict (and costly) climate policies, decide to relocate their carbon-intensive production to countries with weaker environmental regulations. Alternatively, EU products could be replaced by more carbon-intensive imports. The result? Global emissions don’t fall; they just shift geographically, undermining the EU’s climate goals and harming the competitiveness of its industries.

The cornerstone of the EU’s climate policy is the Emissions Trading System (EU ETS), a “cap-and-trade” system operational since 2005. It sets a declining cap on total emissions from covered sectors (like power generation, steel, and cement) and allows companies to trade emission allowances. The price of these allowances (EUAs) has risen significantly, from around €25-35 per tonne of CO2 in 2020 to fluctuating between €60-€90+ in 2024/2025. This creates a real financial incentive for EU companies to decarbonize.

However, this carbon cost puts EU producers at a potential disadvantage against imports from regions without comparable carbon pricing. For years, to prevent leakage, the EU handed out free allowances to at-risk industries. CBAM is the elegant, albeit complex, solution to phase out these free allowances while protecting EU industry. It essentially imposes a carbon price on imports equivalent to what would have been paid had the goods been produced under the EU ETS, creating a level playing field.

The CBAM regulation entered into force in October 2023, with a transitional phase running from October 2023 to December 2025. The definitive system starts in January 2026, coinciding with the phase-out of free allowances for CBAM-covered sectors.

Key Concepts Defined

Let’s demystify the jargon:

- CBAM (Carbon Border Adjustment Mechanism): An EU policy that imposes a carbon cost on imports of certain goods to equalize the carbon price between EU products (subject to the EU ETS) and imports.

- Carbon Leakage: The risk that climate policies in one region lead to increased emissions in another region with laxer rules, negating the global environmental benefit.

- EU ETS (Emissions Trading System): The EU’s cap-and-trade market for greenhouse gas emissions, where companies must surrender allowances for their emissions.

- Embedded Emissions: The total greenhouse gas emissions released during the production of a good, including direct emissions from the production process and indirect emissions from the generation of electricity, steam, and heat consumed.

- CBAM Certificate: A digital certificate purchased by an EU importer to cover the embedded emissions of their imports. The price is linked to the weekly average auction price of EU ETS allowances.

- Authorized CBAM Declarant: The importer of record who is legally responsible for complying with CBAM obligations, including reporting and purchasing certificates.

- Transitional Phase (2023-2025): A period where importers must submit quarterly reports on embedded emissions but do not yet have to pay financially. It’s a “reporting-only” phase for data collection and system testing.

- Definitive Phase (From 2026): The period starting in 2026 when importers must declare the quantity of goods and their embedded emissions annually, surrender the corresponding number of CBAM certificates, and pay the financial adjustment.

- Carbon Price Paid Abroad: A deduction allowed in the CBAM calculation for any explicit carbon price already paid in the country of production (e.g., a national emissions trading scheme or carbon tax).

How It Works (Step-by-Step Breakdown)

Step 1: Determine If Your Goods Are Covered.

CBAM initially applies to imports of goods in six carbon-intensive sectors with high leakage risk:

- Cement

- Iron and Steel

- Aluminium

- Fertilizers

- Electricity

- Hydrogen

Update (2025): The EU is already conducting assessments to potentially expand this list to include chemicals (like ammonia, methanol), polymers (like polyethylene, polypropylene), and further downstream products.

Step 2: Identify Your Role as an Importer (The Declarant).

The legal obligation falls on the EU importer (the “authorized CBAM declarant”). If you are a non-EU producer, your EU customer is legally responsible. However, in practice, you will need to provide them with accurate emissions data.

Step 3: Calculate Embedded Emissions.

This is the most technically demanding part. Emissions must be calculated for each import consignment using one of two methods, in order of preference:

- Actual Emissions Calculation (Preferred): Based on data from the specific installation(s) where the goods were produced. This requires sophisticated monitoring and reporting.

- Default Value (Fallback): If reliable actual data cannot be obtained, a default value will be used. Crucially, these default values are punitive, set at the average emission intensity of the worst-performing 10% of EU installations for that good. This creates a strong incentive to provide actual data.

Step 4: During Transitional Phase (Now – Dec 2025): File Quarterly CBAM Reports.

Every quarter, the declarant must submit a report to their national CBAM authority detailing:

- Total quantity of imported goods (by CN code).

- Total embedded emissions (direct and indirect, separately).

- Any carbon price paid abroad.

Step 5: In Definitive Phase (From Jan 2026): Purchase and Surrender CBAM Certificates.

Annually, by May 31st, the declarant must:

- Submit a definitive CBAM declaration for the previous year.

- Purchase CBAM certificates corresponding to the total embedded emissions declared.

- Surrender these certificates to the national authority.

- The certificate price is based on the weekly average auction price of EU ETS allowances.

Step 6: Account for Carbon Price Paid Abroad and Free Allowances.

The number of CBAM certificates required can be reduced to reflect:

- Any verifiable carbon price already paid in the country of origin.

- During the initial phase-in (2026-2034), a corresponding reduction is made to mirror the phased-out free allowances still being given to EU competitors.

Why It’s Important

CBAM’s importance extends far beyond a new import procedure. It represents a fundamental rewiring of global economic incentives.

1. For the EU:

- Safeguards Climate Ambition: Mitigates carbon leakage, allowing the EU to pursue its aggressive “Fit for 55” (55% emissions reduction by 2030) and net-zero goals without offshoring its industrial base.

- Promotes Global Climate Action: Serves as a powerful diplomatic tool to encourage trading partners to adopt their own robust carbon pricing systems. Why pay a price to the EU when you can set your own and keep the revenue domestically?

2. For Global Businesses & Trade:

- Creates a Level Playing Field: Removes the competitive disadvantage for EU producers investing in clean technologies.

- Embeds Carbon into Financial Decision-Making: Carbon intensity becomes a direct line item on a company’s P&L, making low-carbon production a source of competitive advantage. A steel producer using green hydrogen will face a lower CBAM cost than one using coal.

- Forces Transparency: Requires an unprecedented level of supply chain transparency regarding emissions data, pushing for standardization and verification.

3. For Non-EU Economies:

- A Catalyst for Domestic Policy: Countries heavily exporting to the EU (e.g., Turkey for steel, Russia for fertilizers, China for aluminium) are now incentivized to accelerate their own carbon pricing or clean-tech strategies to protect their export competitiveness.

- Revenue Implications: For some developing economies, CBAM could represent a significant financial outflow. This has sparked debates about climate justice and the need for support.

Real-Life Example (Hypothetical but Realistic): *An Indian fertilizer producer exports 10,000 tonnes of ammonia to the Netherlands. The embedded emissions are 2.5 tonnes of CO2 per tonne of ammonia (actual, efficient plant). Under CBAM in 2027, with an EUA price of €80/tonne, the CBAM cost would be: 10,000 * 2.5 * €80 = €2,000,000. If India had a carbon tax of €30/tonne, this would be deducted: 10,000 * 2.5 * (€80 – €30) = €1,250,000. This massive cost will be a key discussion point in price negotiations between the Indian producer and the Dutch importer.*

Sustainability in the Future

CBAM is a cornerstone of a sustainable future for global trade—a future where environmental externalities are priced into every transaction.

- Driving Global Decarbonization: By making carbon emissions a universal cost, CBAM accelerates investment in clean technologies (electric arc furnaces for steel, CCUS for cement, renewable-based electrolysis for hydrogen) not just in the EU, but globally, as exporters seek to lower their CBAM liability.

- The “Brussels Effect” in Climate Policy: Much like the GDPR set a global standard for data privacy, CBAM has the potential to set a de facto global standard for carbon accounting and pricing. We may see a convergence towards the EU’s methodologies and benchmarks.

- Spillover Effects: The UK is consulting on its own CBAM. Canada is advancing its “Federal Border Carbon Adjustment.” Japan and the US are considering similar measures. We are moving towards a world where “carbon content” could become as important as “country of origin” in trade rules.

- Integration with Other Green Policies: CBAM will interact with the EU Deforestation Regulation (EUDR) and Corporate Sustainability Reporting Directive (CSRD), creating a comprehensive web of sustainability requirements for companies operating in or with the EU.

In my experience, the companies viewing CBAM solely as a compliance burden are setting themselves up for long-term vulnerability. The sustainable future belongs to those who see it as a strategic map, identifying which parts of their supply chain are carbon “hot spots” and innovating to cool them down. This aligns directly with the work we highlight in our focus on sustainable transformation at World Class Blogs.

Common Misconceptions

- Misconception: “CBAM is just a protectionist trade barrier.”

- Reality: While it protects EU industry from carbon leakage, its legal design (and the phasing out of free allowances) is specifically crafted to comply with WTO “national treatment” rules, aiming to equalize conditions, not create an unfair advantage. Its primary stated objective is environmental.

- Misconception: “It’s an EU tax that other countries’ governments will receive.”

- Reality: The revenue from the sale of CBAM certificates flows to the EU budget. It does not go to the exporting country’s government. However, if the exporting country has its own carbon price, that cost paid domestically is deducted from the CBAM obligation.

- Misconception: “Only direct exporters to the EU need to worry.”

- Reality: The impact cascades through supply chains. A South Korean car manufacturer using Chinese steel may find its EU-bound vehicles subject to indirect CBAM costs if the embedded steel emissions aren’t accounted for. This complexity is a core challenge.

- Misconception: “The transitional phase is just a soft start; we can figure it out later.”

- Reality: The transitional phase is a critical data-gathering and relationship-building period. Companies that fail to establish robust data collection systems now will face severe penalties and be forced to use punitive default values in 2026.

- Misconception: “It’s only for huge multinational corporations.”

- Reality: Any EU importer of covered goods, regardless of size, is liable. A small German distributor importing Turkish aluminium profiles must comply in full.

Recent Developments (2024/2025)

- First Quarterly Reports Submitted: The first CBAM quarterly reports for Q4 2023 were due by January 31, 2024. Initial feedback from national authorities indicated widespread under-reporting and errors, highlighting the steep learning curve.

- Refined Default Values Published: The EU has published more granular and sector-specific default values, moving away from the initially proposed simplistic benchmarks.

- IT System Updates: The EU’s central CBAM Transitional Registry has undergone several updates to improve user interface and data validation based on early user experience.

- Expansion Talks Intensify: The 2025 review process is underway, with strong lobbying from EU industries (especially chemicals) to be included in the next phase of expansion. A European Parliament report in early 2025 recommended a “predictable expansion timeline.”

- International Legal Challenges: While no full WTO case has been launched yet, several countries (including China, India, and Russia) have raised formal objections in WTO committees, calling CBAM discriminatory and a potential violation of trade rules.

- Partnering for Capacity Building: The EU has launched technical assistance programs with some developing countries to help build their emissions monitoring, reporting, and verification (MRV) capacities—a key step in addressing equity concerns.

Success Stories (Early Adopters & Strategic Movers)

While the definitive system isn’t yet live, we can see early success in proactive adaptation:

- Norwegian Aluminium Producer Norsk Hydro: A leader in low-carbon aluminium using renewable hydropower. Their product, with embedded emissions as low as 4 kg CO2/kg Al (vs. a global average of ~16 kg), will face a negligible CBAM cost. They are already marketing this as a “CBAM-advantaged” product, securing premium contracts with EU customers. This is a classic “before/after” scenario: before CBAM, their green premium was a hard sell; after CBAM, it becomes a quantifiable financial shield.

- Turkish Steelmaker İÇDAŞ: Has invested in energy efficiency and is piloting the use of hydrogen in production. They are proactively engaging with EU importers to provide verified emissions data, aiming to use the favorable “actual emissions” calculation instead of defaults.

- EU Cement Industry (e.g., Heidelberg Materials): While initially wary, major EU players now support CBAM as it protects their massive investments in carbon capture, utilization, and storage (CCUS) technology. CBAM ensures their higher-cost, low-carbon cement can compete against dirtier imports.

Real-Life Examples & Case Studies

Case Study 1: The Fertilizer Importer in Belgium

- Situation: A Belgian agro-business imports urea fertilizer from Egypt and Russia.

- Challenge: The Egyptian plant uses efficient natural gas, while the Russian plant uses older, coal-based technology. The carbon intensity differs dramatically.

- CBAM Action: The importer cannot simply use an average. They must collect separate, verified emissions data from each specific production plant. They negotiate new contracts requiring suppliers to provide quarterly emissions data certified by an accredited verifier. They start modeling the future cost impact, finding that Russian urea may become uncompetitive, prompting a strategic shift in sourcing.

Case Study 2: The Automotive Tier-1 Supplier in Slovakia

- Situation: A supplier produces car bodies for EU OEMs, using imported Chinese steel coils.

- Challenge: The CBAM cost on the embedded emissions in the steel is a direct cost for the steel importer, but it will inevitably be passed down the chain, increasing the supplier’s raw material costs.

- CBAM Action: The supplier’s procurement team must now add “CBAM-adjusted cost” to their supplier evaluation matrix. They work with their logistics and finance teams to understand the declarant obligations. They also engage with their customer (the carmaker) in discussions about future cost-sharing and the potential to switch to greener, potentially EU-produced, steel to mitigate long-term risk.

Conclusion and Key Takeaways

The EU’s Carbon Border Adjustment Mechanism is not a distant future concept; it is operational law. It marks the decisive moment when climate policy stopped being a domestic concern and became a foundational element of international trade architecture.

Key Takeaways:

- CBAM is Here to Stay and Grow: It began with six sectors but will almost certainly expand in scope and complexity. Building compliance expertise now is an investment.

- Data is the New Currency: The ability to accurately measure, report, and verify the carbon footprint of your products is transitioning from a nice-to-have CSR metric to a critical commercial and financial imperative.

- Supply Chain Relationships Will Change: CBAM forces unprecedented collaboration and data sharing between importers and their foreign suppliers. Trust and transparency are paramount.

- Low-Carbon Production is a Competitive Edge: CBAM turns carbon efficiency into direct cost savings and market advantage. Investments in clean technology are no longer just ethical; they are economically rational.

- Think Strategically, Not Just Compliantly: Beyond filling out forms, use CBAM as a lens to review your entire value chain, identify carbon and cost risks, and innovate for resilience in a decarbonizing global economy.

The businesses and economies that thrive in this new era will be those that see CBAM not as a wall, but as a compass—pointing decisively towards the sustainable, transparent, and efficient future of global commerce. For more insights on navigating complex global systems, explore our other analyses on World Class Blogs.

FAQs (20–25 detailed Q&A)

1. Who exactly needs to comply with CBAM?

The legal obligation falls on the EU importer (the “authorized CBAM declarant”) of covered goods. If you are a non-EU producer, your EU customer is responsible for compliance, but they will require detailed emissions data from you.

2. What happens if I don’t comply during the transitional phase (2023-2025)?

Non-compliance can result in significant financial penalties. Authorities can impose fines of €10 to €50 per tonne of unreported emissions. Furthermore, persistent non-compliance could lead to being forced to use punitive default values in the definitive phase.

3. How is the price of a CBAM certificate determined?

The price is not fixed. It is based on the weekly average auction price of EU ETS allowances (EUAs). The CBAM authority will publish this price regularly. Declarants will purchase certificates at this fluctuating price.

4. Can I use verified emissions data from other standards (e.g., GHG Protocol)?

The EU CBAM has its own specific calculation methodologies and reporting templates. While the underlying data you collect (e.g., fuel consumption, process data) is similar, you must translate it into the format prescribed by the EU Implementing Regulation. It’s advisable to use a verifier familiar with both CBAM and international standards.

5. What’s the difference between direct and indirect emissions for CBAM?

- Direct Emissions: Emissions from the production processes of the goods themselves (e.g., chemical reactions in cement production, combustion in a steel furnace).

- Indirect Emissions: Emissions from the generation of electricity, steam, and heat that is consumed in the production process. For most initial CBAM goods, only direct emissions are fully covered, except for electricity and, crucially, hydrogen. The rules for indirect emissions in other sectors are still being clarified.

6. My country has a carbon tax. How does that reduce my CBAM cost?

If you can provide verifiable proof of a carbon price paid in the country of production (e.g., a tax receipt, evidence of surrendering allowances in a national ETS), the CBAM declarant can deduct this amount from the total number of CBAM certificates they need to surrender. This prevents double-charging.

7. Will CBAM apply to goods that are further processed outside the EU before being imported?

The current rules focus on “simple” goods. However, for some complex goods (like screws made from imported steel), there are specific rules for calculating emissions for the precursor materials. This is a highly technical area. The general principle is that the embedded emissions from all precursor materials subject to CBAM must be included.

8. How do I find my national CBAM competent authority?

The European Commission maintains a list on its official website. Each EU member state has designated an authority (often the environment ministry, customs agency, or tax administration). You must register with the authority in the member state where you are established or where the goods are first released for free circulation.

9. What software or tools are available for CBAM reporting?

The EU provides a free, centralized CBAM Transitional Registry for submitting quarterly reports. For definitive reporting and complex emissions calculations, many specialized software providers (like SAP, Sphera, Persefoni) and consulting firms are developing CBAM modules. For a foundational business strategy, resources like Sherakat Network’s guide to strategic alliances can be useful in building the partnerships needed for compliance.

10. Does CBAM violate World Trade Organization (WTO) rules?

The EU designed CBAM carefully to align with WTO principles (like “national treatment”). However, it remains legally untested. Several countries have raised disputes. A future WTO panel will ultimately decide, but any ruling is years away. Businesses must operate on the assumption that CBAM is valid and binding.

11. What about small and medium-sized enterprises (SMEs) that import?

The regulation makes no exemption for SMEs. However, the EU and member states are offering guidance and support programs. SMEs should engage with industry associations, seek expert advice, and potentially collaborate to share compliance resources.

12. How does CBAM relate to the EU’s Corporate Sustainability Reporting Directive (CSRD)?

They are complementary. CSRD requires large companies to publicly report on their sustainability impacts, including Scope 3 (value chain) emissions. The data collected for CBAM (especially from suppliers) will be invaluable for accurate CSRD reporting. They form two parts of the EU’s broader sustainability data ecosystem.

13. What if the production process uses renewable energy? How is that accounted for?

If you use renewable energy (e.g., a solar PV plant powering your aluminium smelter), you must provide evidence (e.g., Power Purchase Agreements, guarantees of origin). This will result in lower or even zero indirect emissions in your calculation, significantly reducing your CBAM liability.

14. Are there any exemptions?

Goods imported in small quantities (valued below €150) are exempt. Imports from countries fully integrated into the EU ETS (Iceland, Liechtenstein, Norway) or who have linked their ETS to the EU’s (Switzerland) are also exempt, as they are already subject to an equivalent carbon price.

15. What happens after 2034?

By 2034, the free allocation of allowances under the EU ETS for CBAM-covered sectors will be completely phased out. From that point, CBAM will apply in full, with no adjustment for free allowances, representing the final, complete level playing field.

16. How will CBAM be enforced?

National authorities will conduct checks and audits. They can request supporting documentation, verify calculations, and inspect premises. Customs authorities will also play a role, as CBAM declarations will be linked to customs procedures for release of goods.

17. Can I trade or bank CBAM certificates?

Yes, to some extent. Declarants can sell back to the authority a limited number of surplus certificates (up to one-third of their total purchased in a year) at the purchase price. This provides some flexibility if imports are lower than forecast.

18. What’s the single biggest mistake importers are making right now?

Underestimating the complexity of data collection and assuming their suppliers are ready. The biggest mistake is waiting. The time to engage with your supply chain, audit your data gaps, and run pilot calculations is now, during the transitional phase.

19. Is the UK implementing its own CBAM?

Yes, the UK government has consulted on a UK CBAM, expected to be implemented by 2027. It will likely cover similar sectors and align broadly with the EU model, but with key differences (e.g., linked to the UK ETS price). Businesses trading with the UK must prepare for a similar regime.

20. Where can I get official, updated information?

The European Commission’s Directorate-General for Taxation and Customs Union (DG TAXUD) website is the primary source. Your national competent authority’s website is also essential for country-specific guidance.

21. How does CBAM affect countries in the Global South?

It poses a significant challenge. Many lack the technical capacity for sophisticated emissions monitoring and have carbon-intensive export industries. There are concerns about unfair burden and revenue loss. The EU is offering some technical assistance, but calls for more support and a just transition framework are loud, similar to discussions around broader global development found in our Nonprofit Hub category.

22. Will this make everything imported into the EU more expensive?

It will make carbon-intensive goods more expensive. Low-carbon imports will see little to no increase. The goal is to shift demand towards cleaner products, rewarding producers who have invested in decarbonization.

23. What about recycled materials (e.g., scrap-based steel)?

Goods produced from recycled materials typically have a much lower embedded emissions footprint. The CBAM calculation methodologies account for this, providing a significant advantage to circular economy business models.

24. Can consultants or third parties act as the authorized declarant?

Generally, the liability stays with the importer of record. However, they can use a representative to perform the technical and administrative tasks, but the legal responsibility cannot be fully outsourced.

25. How does this fit with broader geopolitical tensions?

CBAM adds a new layer to EU-China and EU-Russia relations. It’s seen as an assertion of “regulatory power.” Some countries may view it as economic coercion. It will undoubtedly be a point of negotiation in future trade agreements and diplomatic talks, intersecting with the field of global affairs & policy.

About Author

Sana Ullah Kakar is a Senior Trade Policy and Sustainability Advisor with over 15 years of experience navigating the intersection of international regulations, supply chains, and environmental strategy. Having worked with multinational corporations, industry associations, and EU institutions, they bring a pragmatic, real-world perspective to complex frameworks like CBAM. They are a frequent contributor to World Class Blogs, demystifying global economic trends for professionals and curious learners alike. Connect with our team through our Contact Us page.

Free Resources

- European Commission CBAM Official Page: The primary legal and guidance repository.

- CBAM Transitional Registry User Manual: Essential for navigating the reporting platform.

- Industry Association Toolkits: Many sector-specific associations (e.g., EUROFER for steel, CEMBUREAU for cement) have developed detailed guidance for their members.

- World Bank Carbon Pricing Dashboard: Excellent for understanding carbon prices paid abroad in different jurisdictions.

- For understanding the mental model shifts required in modern business, The Daily Explainer’s guide to Mental Health offers parallels in adapting to new systemic pressures.

- To build the partnerships necessary for CBAM compliance, consider the frameworks in Sherakat Network’s guide to Business Alliances.

Discussion

We want to hear from you! Is your business already preparing for CBAM? What has been your biggest challenge: data collection, supplier engagement, or understanding the regulations? Do you see CBAM as a threat or an opportunity for your industry? Share your thoughts and questions in the comments below. Let’s build a community of knowledge to navigate this new era of trade together.

For more deep dives into transformative topics across technology, business, and global affairs, explore the full range of content in our Blogs category.